Make the claim pay for the whole roof

After a Michigan storm, the roof damage is only half the battle. The other half is the claim, and that is where a lot of Sterling Heights owners come up short. The insurer's first offer can be lighter than the cost of a sound new roof, and a claim that is filed loose can be denied or paid out as plain old wear. Proving the loss to an adjuster is a separate skill from the storm damage roof repair itself. Done well, it is what moves a thin first number toward a fair one.

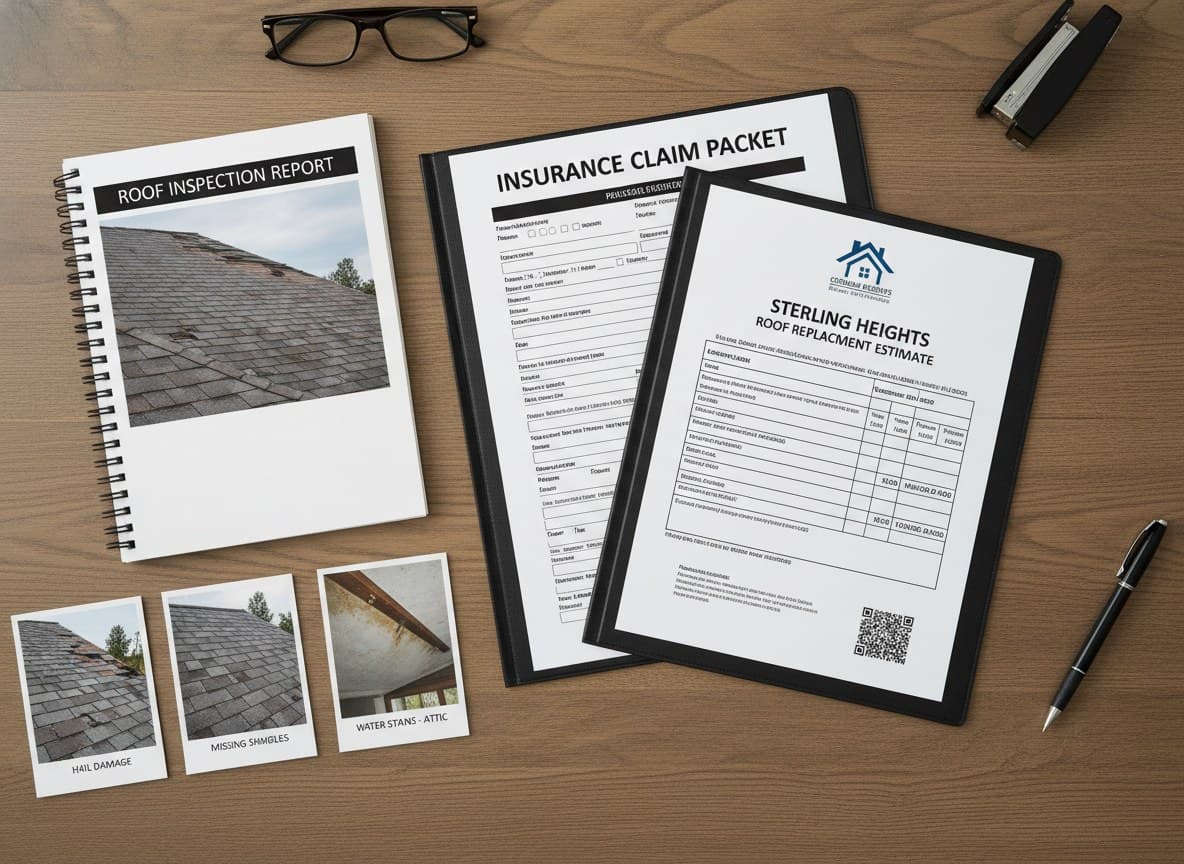

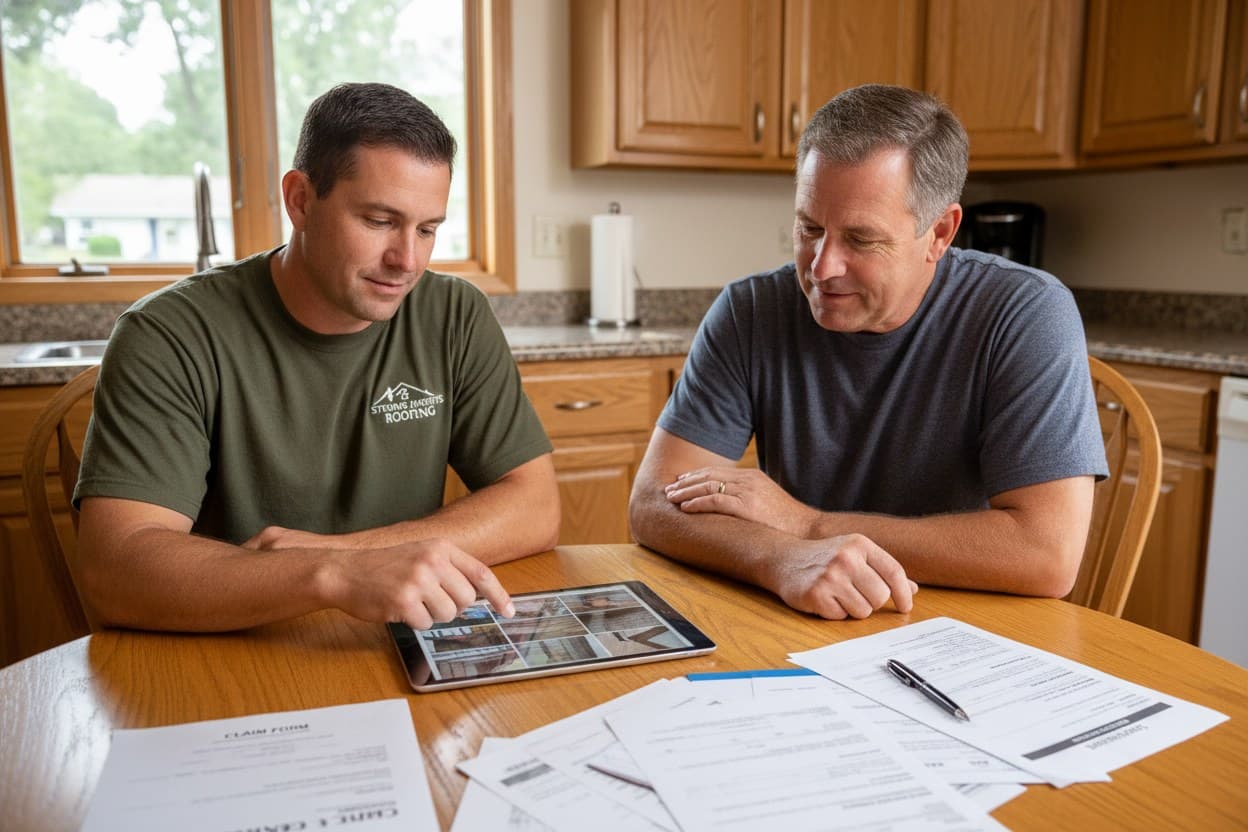

Claim help sits next to the repair work, not on top of it. It starts with a careful inspection where a roofer records each bruised shingle, torn tab, and bent vent with dated photos. The homeowner opens the claim, and the insurer sends an adjuster out to size up the loss. The most useful step is having a roofer on the roof when that adjuster climbs up, so real damage does not get read as age. When the insurer's scope skips flashing, vents, or code work, the roofer answers with a supplement and the proof to back it.

- Every hail mark and lifted shingle gets logged with dated photos.

- A roofer stands with the adjuster on the roof, not the driveway.

- Straight talk on what the deductible covers and what it will not.

- Flashing, vents, and code items get added back through a supplement.

- A detailed scope leaves the adjuster little room to pay short.

Sterling Heights takes the summer storms that roll across Macomb County and the wet snow that loads roofs all winter. The insurers that write policies here have seen those losses for years and know which claims to push back on. A roofer who works this area knows the same weather and often the same adjusters. They can speak to Michigan code, ice dam damage at the eaves, and what a fair scope should hold for a home in this county. We route your call to a roofer who handles storm claims across Sterling Heights and the rest of Macomb County.

Before you cash a first check or sign with anyone, let a roofer read both the damage and the insurer's scope. The inspection and claim review cost nothing, and no one will push you to sign that day. Call today and a vetted Sterling Heights roofer will look at the roof and the paperwork this week.